Supply and Demand in Today’s Market [INFOGRAPHIC]

KCM • March 14, 2022

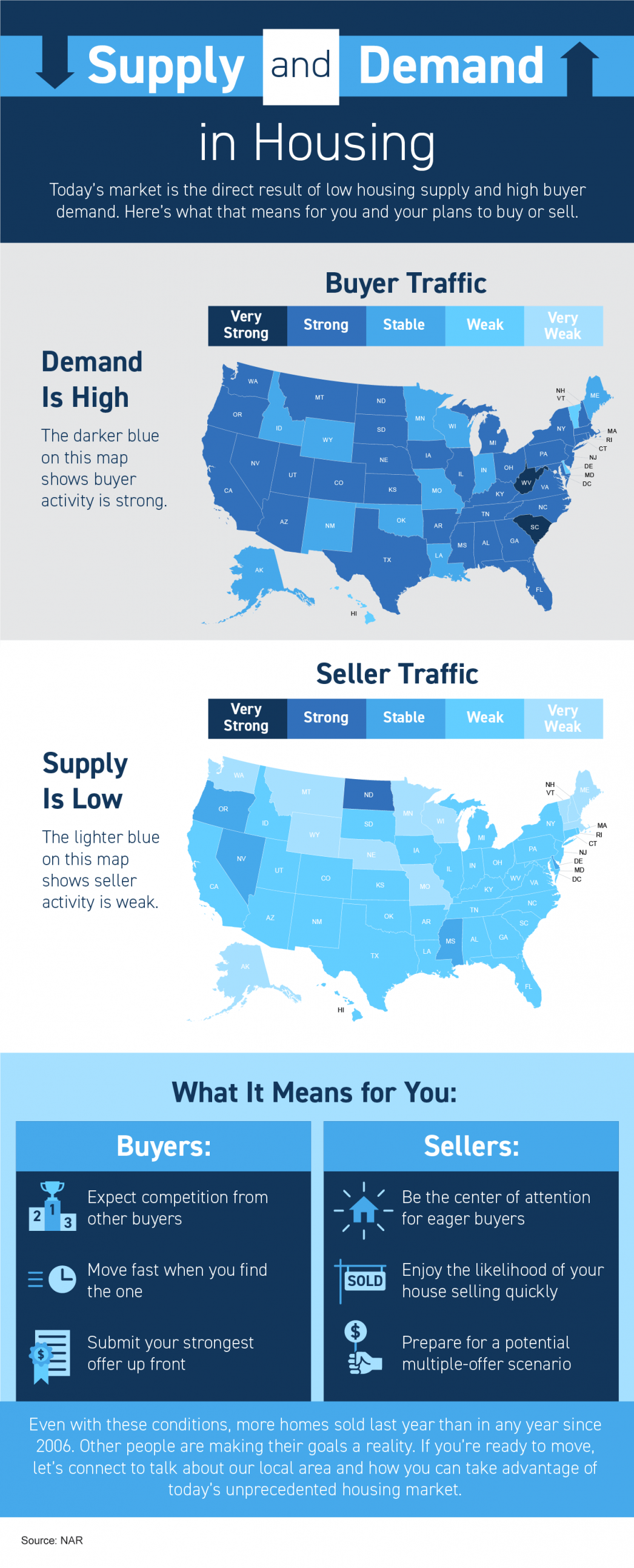

Supply and Demand in Today’s Market [INFOGRAPHIC]

Some Highlights

- Today’s housing market is the direct result of low supply and high buyer demand. Here’s what that means for you and your plans to buy or sell.

- For buyers, expect competition, be ready to move fast, and be prepared to submit your strongest offer. For sellers, know your house will be the center of attention and that it’ll likely sell quickly and get multiple offers.

- If you’re ready to move, let’s connect to talk about our local area and how you can take advantage of today’s unprecedented housing market.

Share this post

Why Staging Your House Could Pay Off This Spring Selling your house this season? You’ve probably heard you should stage it before it hits the market. But what does that really mean – and is it worth the effort? The short answer is “yes,” especially right now. With more houses for sale this year, you’re likely wondering how to make the most money possible without your house sitting on the market. The answer is staging. It can help your house stand out, bring in stronger offers, and sell faster . As Nadia Evangelou, Principal Economist at the National Association of Realtors (NAR), puts it: “Staging matters. Preparing the home to be ‘buyer-ready’ attracts more buyers, especially now that inventory has increased.” Here's what staging actually involves and what it could do for your sale. What Is Home Staging? Home staging is the process of preparing your house, so it appeals to as many buyers as possible . That usually means decluttering, deep cleaning, rearranging furniture, and adding simple touches that help each room feel bright, open, and welcoming. The goal is to help buyers fall in love with the space and picture themselves living there , which makes them more likely to make an offer. Why Staging Is Worth the Effort Staged houses tend to perform better on almost every metric that matters when you sell. According to Redfin, staged homes have been shown to sell up to 73% faster than unstaged homes. And they often close in under a month, compared to anywhere from two to three months for vacant ones. There’s also a strong return on the money you spend. The Home Staging Institute says mid-level staging can deliver a 350% return on investment. On a $400k home, that turns the typical $4k cost into roughly $18k in added value when you sell (see graph below): By that estimate, that’s an extra potential profit of about $14k – a meaningful boost when you’re trying to maximize what you walk away with at closing. Your Staging Options And just in case you’re seeing that $4k upfront investment above and thinking, “I’m not going to spend that,” here’s what you should know. Staging doesn’t always have to mean hiring a full crew or filling your house with rented furniture. There are a few different paths you can take, depending on your budget and timeline. So, you could spend a lot less and still get a good return. Here are a few options: Professional staging. A stager handles everything from layout to décor, often bringing in their own inventory. According to the Home Staging Institute, costs typically range from $500 to $5k or more, depending on the size of your house. Virtual staging. Digital furniture and styling are added to your listing photos, which can be a budget-friendly option for vacant houses. DIY staging. If your budget is tight and your home only needs minor updates, decluttering, deep cleaning, and arranging furniture for flow can still make a real difference. Your agent can help you figure out which approach fits your house, your market, and your goals. Agents see what buyers respond to in open houses and showings every week, so they can give you specific, personalized recommendations on what’s worth your time and money (and what isn’t). That way you can get the most bang for your buck – no matter your budget. Bottom Line With more homes for sale right now, making a strong first impression matters. Staging can help your house sell faster and for more – and there's an option for almost every budget. If you’re getting ready to list, let’s talk about what level of staging makes sense for your house and make a plan for attracting the right buyers.

Could Co-Buying Be the Answer for Some First-Time Buyers? For a lot of would-be first-time buyers , affordability is the thing that’s standing in the way. But some buyers are getting creative and finding a way to still make the numbers work – and that’s through co-buying . The Dream Is Still Alive. The Math Just Isn’t Working for Everyone. Young people haven’t given up on the dream of owning a home – not even close. According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation. The problem? 73% of Gen Z and millennial buyers cite affordability as the reason for not making homeownership a priority. And it shows. First-time buyers now make up just 21% of all home purchases , the lowest share since the National Association of Realtors (NAR) started tracking the data in 1981. But still, some buyers are making it happen. And a portion of them are turning to co-buying to get their foot in the door. So, What’s Co-Buying? Co-buying means purchasing a home with someone else, like a friend, sibling, or unmarried partner. You combine incomes, split the down payment, and share monthly costs. For some people, it’s a creative way to turn “someday” into a concrete move-in date that’s just around the corner. And it's catching on fast, just look at where things stand today. According to CoBuy.io , 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers (see graph below): Why It Works Here are just a few of the top reasons buyers are going this route, according to NerdWallet: Quicker path to homeownership: If owning a home is a serious goal for you, buying with someone else can help make that reality on a shorter timeline. Two or more people can save up a down payment a lot faster than one. That’s less time waiting and more time building equity in a place that’s yours. More purchasing power: With multiple incomes going toward the home purchase, you might be able to afford a nicer home or live in a more popular neighborhood. Sometimes teaming up means getting the home you actually want, not just the one you can barely afford on your own. Easier loan qualification: Added income from more than one buyer can also help with your debt-to-income (DTI) ratio, which the lender will calculate based on all the borrowers. Lower housing costs: Splitting up a mortgage payment multiple ways could maybe even make owning less expensive than renting . Plus, sharing costs can make repairs or renovations more manageable, too. Things To Keep in Mind If you’re considering going this route, there are some things you’ll want to think over. For starters, co-buying works best with people you trust and share financial goals with. So, before moving forward, make sure everyone agrees on how costs are split, who handles what, and what happens if one person wants to sell down the road. That’s why a written co-ownership agreement can be a smart move. It keeps everyone on the same page and helps avoid headaches down the line. Think of it less like a legal formality and more like a game plan for your new investment. Bottom Line Affordability challenges are real, but they don't have to mean waiting indefinitely. Co-buying is helping some first-time buyers stop waiting and start putting down roots. If you're curious whether it could work for your situation, let's talk. Reach out today and let's figure out your path to homeownership together.

The Secret To Selling Fast, No Matter the Market When you put your house on the market, you don’t just want it to sell. You want it to sell fast . But the thing is, nationally, it’s taking a little longer to sell lately. And that slowdown can feel frustrating if you want a fast process. Here’s what you need to realize. In every market right now, there’s one clear exception: Well-priced, well-presented homes are still selling, and it’s often faster than you’d expect. If you can tap into that, you can still set yourself up to move quickly, too. Here’s how to get it done. How Long It Takes To Sell Today According to Realtor.com, homes are selling in about 52 days right now. That’s how long the process takes from the day it hits the market until closing day . And while that may sound slow to you, it’s not slow. It’s normal. That’s because it’s pretty much right in line with what it was during the last normal years in the market (see 2018-2019 in the graph below): It just feels slow when you’re eager to move – or when you think back a few years to when homes seemed to sell almost instantly. But here’s what matters most. The market is normalizing. Not at a standstill. This is the norm for timing from start to finish. You may have an accepted offer in hand even faster than this. Markets Where Homes Still Sell Quickly, Even Now Zillow says the typical home will go “pending” or “under contract” in 19 days. Some homes even see it happen in as little as 7 days. It just depends on where you are – and how you prep your house. So, don’t let the slowing pace of sales stress you out. Homes can still sell fast, if they’re positioned right. Just to show you, here’s a quick look at some of the markets that are moving faster than the norm, according to Zillow (see map below). This’ll show you how different it can be based on where you live. The key things you need to remember when looking at this visual: It varies a lot based on where you live. Within the same state, individual neighborhoods or pockets may sell much faster than the norm. Even in slower moving states, you can still sell quickly. As the map shows, in those places there are still homes that go under contract in as little as a week. So don’t worry about if your state made either list. As Orphe Divounguy, Senior Economist at Zillow, says: “The cream of the crop is still selling fast, even in markets that have slowed considerably . . .” The Big Reasons Some Homes Sit, and Some Sell Fast And here’s the big secret. While location can definitely play a role, it’s not just about location. It’s about strategy. Today’s buyers are paying attention to condition . They’re comparing photos, upgrades, layout, location, and price. And they’re choosing homes that feel move-in ready and well worth the value . The homes that check those boxes? They’re not sitting for long – no matter where they are. As the Wall Street Journal (WSJ) explains: “. . . some homes are still flying off the shelves. These houses are often in the Midwest or Northeast, where the lack of new construction keeps a lid on supply. Certain homes in other markets are selling quickly, too, often when a home is move-in ready .” Because in any market – hot or not – if a home is overpriced , needs too much work, or just doesn’t meet current buyer expectations, it’s not going to sell. In this market, the sellers who win are the ones who get real about their house. They’re honest about how their home compares to other listings, realistic about price, and they work with an agent who truly understands today’s market and what it takes to sell. When your agent knows how to price strategically, spotlight the strengths of your home, and move quickly when the market gives clear signals, that’s when the results follow. Bottom Line Today's housing market rewards the right strategy. Because even in a slower area, the homes that are priced realistically and positioned well are still selling – sometimes faster than you may expect. Let’s connect if you’re ready to make yours one of them.