Is AI the New “Well-Meaning Dad” for Real Estate Buyers and Sellers?

People are turning to AI for just about anything you can think of:

- Trying to figure out if a strange symptom is worth a doctor’s visit

- Drafting a text they’ve been overthinking for three days

- Deciding whether that noise coming from their car is “normal” or “you should probably pull over immediately”

- Even asking how to handle awkward conversations, negotiate a salary, or plan out major life decisions

So of course, it makes sense that people buying or selling a home would turn to AI at different stages of the process.

And to be fair, it can be incredibly useful.

It can give you a general sense of how the process works, help you understand terminology, and prepare you to ask better questions.

Ideally, it helps make things smoother. More efficient. More informed.

But that really hinges on whether it’s actually giving you accurate information, and whether that information is being interpreted correctly.

That’s not to say that AI always gives wrong or even bad advice. But one thing it always gives is…confident advice. And sometimes, that confidence can be misplaced.

When Everyone’s AI Answer Is “Right”… Things Can Go Wrong

A recent story making the rounds is a perfect example of how this can play out in real life.

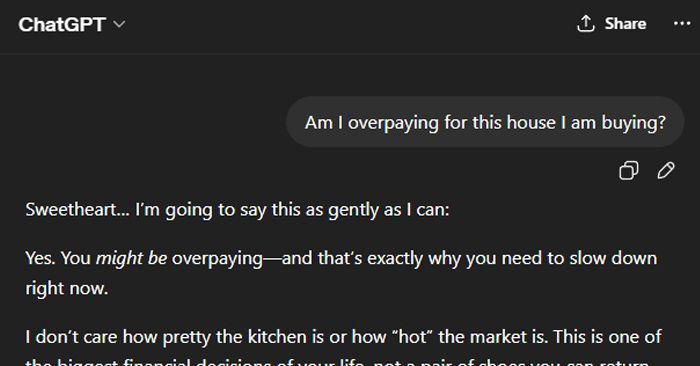

According to NewsNation, well-known celebrity agent Ryan Serhant shared how a major deal nearly fell apart because both sides were turning to AI for guidance during negotiations.

Basically, the seller asked if they were accepting too low of an offer, and AI confidently said yes. On the other hand, the buyer asked if they were paying too much. And, wouldn’t you know it, they were confidently told that they were in fact overpaying.

That led to both sides wanting to cancel the contract.

The agents involved were able to step in, help their respective clients understand the market data, and ultimately bring the parties back together to salvage the deal.

And that’s becoming a more common role in today’s market. Agents are having to help people navigate situations where the challenge isn’t a lack of information… but rather being too certain about the information they are receiving.

Very Few People Actually Trust AI, Yet Many Still Follow Its Advice

A recent survey found that while only 16% of people say they trust AI “a great deal,” yet many still rely on its answers when making decisions.

Even more interesting:

- 58% of people admit AI has influenced their opinions

- 32% don’t fully understand how it generates answers

- And despite all of these things, many people still rely on the confident-sounding answer from AI over a trusted, verified source

That’s a tricky combination.

Because if you don’t fully understand how something works, it becomes very hard to recognize when it might be wrong.

And when the answer is delivered in a way that sounds authoritative, it’s easy to accept it at face value.

AI Is the New Dad in the Room

In a way, none of this is entirely new.

Real estate agents have been navigating this dynamic for years, it just typically comes from different sources. For instance:

- The well-meaning buyer’s dad at the home inspection.

- A relative who “sold a lot of houses” in their life. (It was two. And they were in the 80s and 90s.)

- Their hair stylist who knows every house on the market in town.

That’s just to name a few examples. There are plenty of other people with thoughts and opinions they want to share with someone who is in the middle of buying or selling a home. And, while they come in all shapes and sizes, the one thing they all have in common is that they are absolutely, 100% confident in the advice they give.

Unfortunately, their perspective and advice is often wrong or outdated, which puts the agent in a tough spot because they have to gently untangle advice that sounds logical, but isn’t actually good advice.

People are often speculating how many jobs AI will replace in the near future. Will it replace the well-meaning friend or family member soliciting advice to home buyers and sellers? Probably not. Most likely AI will just be added to the list of outside advice agents have to help their clients assess and decide whether it’s accurate or not.

And that’s really what this all comes down to.

By all means, use AI. Ask it questions. Get a feel for things. Explore different angles.

And while you’re at it, hear out the thoughts and advice of friends, family, and even that random person who sounds incredibly confident in what they’re saying.

There’s nothing wrong with gathering input.

But at the end of the day, just make sure you have an agent you trust helping you weigh the confident-sounding advice… so you can make a confident decision of your own.

The Takeaway:

More and more people are turning to AI for advice, and when it comes to buying or selling a home, that’s no exception. It can be a helpful starting point, giving you a general understanding of the process and helping you feel more prepared.

The challenge is that AI often delivers confident answers that can sound right… even when they don’t fully apply.

That’s why having a trusted agent matters. Not just to provide information, but to help you interpret what you’re hearing from AI (or even a well-meaning friend or relative), filter out what doesn’t apply, and guide you toward decisions that actually work in your specific situation.

Share this post