How Owning a Home Grows Your Wealth with Time [INFOGRAPHIC]

KCM • June 24, 2023

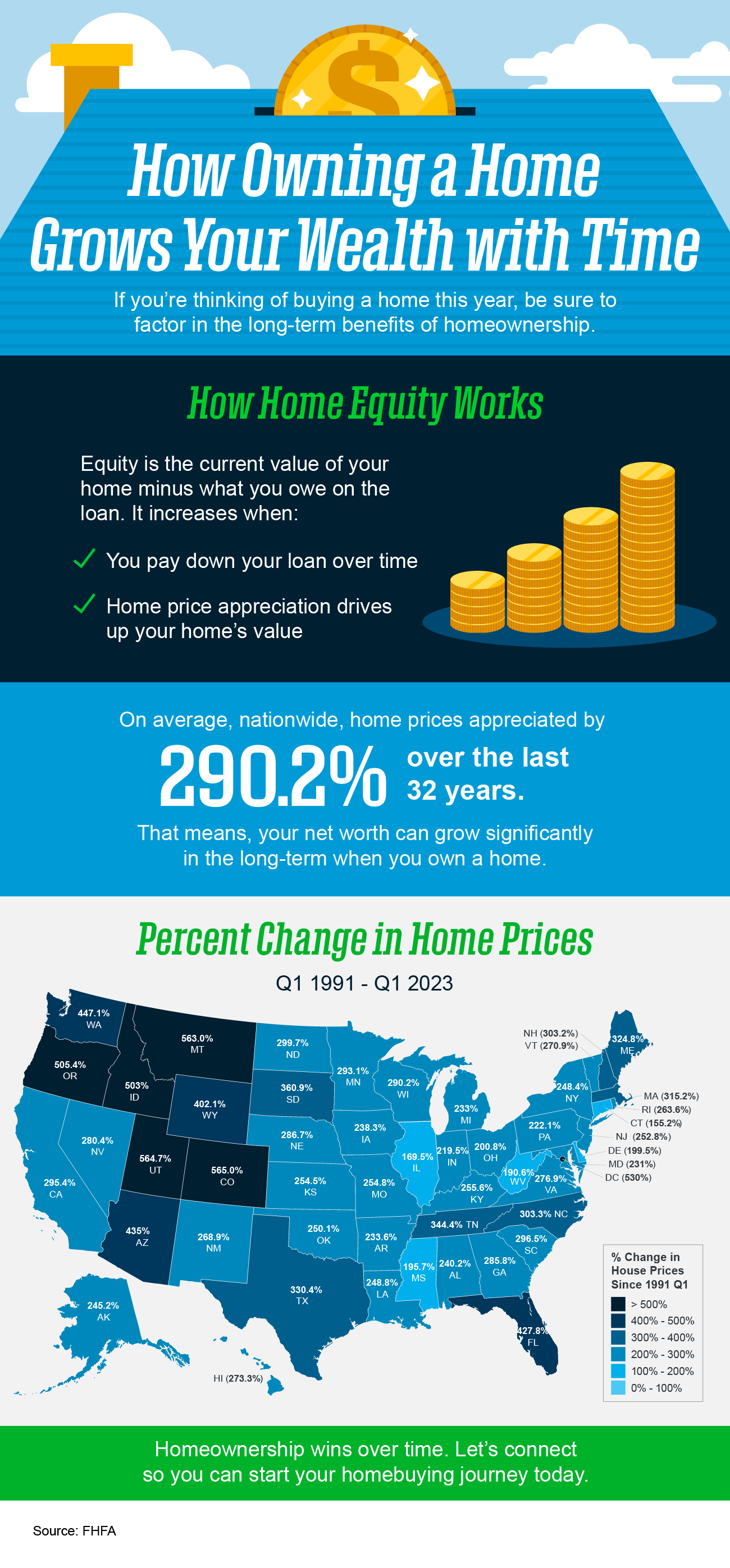

Some Highlights

- If you’re thinking of buying a home this year, be sure to factor in the long-term benefits of homeownership.

- Over time, homeownership allows you to build equity. On average, nationwide home prices appreciated by 290.2% over the last 32 years.

- That means your net worth can grow significantly in the long term when you own a home. Let’s connect so you can start your homebuying journey today.

Share this post

Could Co-Buying Be the Answer for Some First-Time Buyers? For a lot of would-be first-time buyers , affordability is the thing that’s standing in the way. But some buyers are getting creative and finding a way to still make the numbers work – and that’s through co-buying . The Dream Is Still Alive. The Math Just Isn’t Working for Everyone. Young people haven’t given up on the dream of owning a home – not even close. According to FirstHome IQ, homeownership still ranks among the top life goals for the next generation. The problem? 73% of Gen Z and millennial buyers cite affordability as the reason for not making homeownership a priority. And it shows. First-time buyers now make up just 21% of all home purchases , the lowest share since the National Association of Realtors (NAR) started tracking the data in 1981. But still, some buyers are making it happen. And a portion of them are turning to co-buying to get their foot in the door. So, What’s Co-Buying? Co-buying means purchasing a home with someone else, like a friend, sibling, or unmarried partner. You combine incomes, split the down payment, and share monthly costs. For some people, it’s a creative way to turn “someday” into a concrete move-in date that’s just around the corner. And it's catching on fast, just look at where things stand today. According to CoBuy.io , 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers (see graph below): Why It Works Here are just a few of the top reasons buyers are going this route, according to NerdWallet: Quicker path to homeownership: If owning a home is a serious goal for you, buying with someone else can help make that reality on a shorter timeline. Two or more people can save up a down payment a lot faster than one. That’s less time waiting and more time building equity in a place that’s yours. More purchasing power: With multiple incomes going toward the home purchase, you might be able to afford a nicer home or live in a more popular neighborhood. Sometimes teaming up means getting the home you actually want, not just the one you can barely afford on your own. Easier loan qualification: Added income from more than one buyer can also help with your debt-to-income (DTI) ratio, which the lender will calculate based on all the borrowers. Lower housing costs: Splitting up a mortgage payment multiple ways could maybe even make owning less expensive than renting . Plus, sharing costs can make repairs or renovations more manageable, too. Things To Keep in Mind If you’re considering going this route, there are some things you’ll want to think over. For starters, co-buying works best with people you trust and share financial goals with. So, before moving forward, make sure everyone agrees on how costs are split, who handles what, and what happens if one person wants to sell down the road. That’s why a written co-ownership agreement can be a smart move. It keeps everyone on the same page and helps avoid headaches down the line. Think of it less like a legal formality and more like a game plan for your new investment. Bottom Line Affordability challenges are real, but they don't have to mean waiting indefinitely. Co-buying is helping some first-time buyers stop waiting and start putting down roots. If you're curious whether it could work for your situation, let's talk. Reach out today and let's figure out your path to homeownership together.

The Secret To Selling Fast, No Matter the Market When you put your house on the market, you don’t just want it to sell. You want it to sell fast . But the thing is, nationally, it’s taking a little longer to sell lately. And that slowdown can feel frustrating if you want a fast process. Here’s what you need to realize. In every market right now, there’s one clear exception: Well-priced, well-presented homes are still selling, and it’s often faster than you’d expect. If you can tap into that, you can still set yourself up to move quickly, too. Here’s how to get it done. How Long It Takes To Sell Today According to Realtor.com, homes are selling in about 52 days right now. That’s how long the process takes from the day it hits the market until closing day . And while that may sound slow to you, it’s not slow. It’s normal. That’s because it’s pretty much right in line with what it was during the last normal years in the market (see 2018-2019 in the graph below): It just feels slow when you’re eager to move – or when you think back a few years to when homes seemed to sell almost instantly. But here’s what matters most. The market is normalizing. Not at a standstill. This is the norm for timing from start to finish. You may have an accepted offer in hand even faster than this. Markets Where Homes Still Sell Quickly, Even Now Zillow says the typical home will go “pending” or “under contract” in 19 days. Some homes even see it happen in as little as 7 days. It just depends on where you are – and how you prep your house. So, don’t let the slowing pace of sales stress you out. Homes can still sell fast, if they’re positioned right. Just to show you, here’s a quick look at some of the markets that are moving faster than the norm, according to Zillow (see map below). This’ll show you how different it can be based on where you live. The key things you need to remember when looking at this visual: It varies a lot based on where you live. Within the same state, individual neighborhoods or pockets may sell much faster than the norm. Even in slower moving states, you can still sell quickly. As the map shows, in those places there are still homes that go under contract in as little as a week. So don’t worry about if your state made either list. As Orphe Divounguy, Senior Economist at Zillow, says: “The cream of the crop is still selling fast, even in markets that have slowed considerably . . .” The Big Reasons Some Homes Sit, and Some Sell Fast And here’s the big secret. While location can definitely play a role, it’s not just about location. It’s about strategy. Today’s buyers are paying attention to condition . They’re comparing photos, upgrades, layout, location, and price. And they’re choosing homes that feel move-in ready and well worth the value . The homes that check those boxes? They’re not sitting for long – no matter where they are. As the Wall Street Journal (WSJ) explains: “. . . some homes are still flying off the shelves. These houses are often in the Midwest or Northeast, where the lack of new construction keeps a lid on supply. Certain homes in other markets are selling quickly, too, often when a home is move-in ready .” Because in any market – hot or not – if a home is overpriced , needs too much work, or just doesn’t meet current buyer expectations, it’s not going to sell. In this market, the sellers who win are the ones who get real about their house. They’re honest about how their home compares to other listings, realistic about price, and they work with an agent who truly understands today’s market and what it takes to sell. When your agent knows how to price strategically, spotlight the strengths of your home, and move quickly when the market gives clear signals, that’s when the results follow. Bottom Line Today's housing market rewards the right strategy. Because even in a slower area, the homes that are priced realistically and positioned well are still selling – sometimes faster than you may expect. Let’s connect if you’re ready to make yours one of them.

If you’ve ever bought a home before, you’re probably familiar with the advice that agents give their clients: don’t make any big purchases while you’re in the middle of house hunting. “Big purchases” can mean a lot of things—opening new lines of credit, splurging on furniture, committing to a pricey vacation, or upgrading appliances. And, of course, the one agents mention the most…a new car. Even with that warning, it’s easy to see how some buyers slip. Life happens. Sometimes it’s a planned purchase, sometimes it’s impulsive, and sometimes it’s just unavoidable. A new car can sneak into the budget without realizing its ripple effects. Yet these decisions can dramatically impact how much home a buyer can afford, or even whether they qualify for a mortgage at all. Cars aren’t exactly optional for most people. You can’t always time a broken-down engine or a growing family’s need for extra space to line up with your home buying schedule. And some buyers may have purchased a vehicle months before they even began house hunting, not fully aware of the impact it could have on their homebuying power. But to the degree that it is in your control, understanding the numbers can make a huge difference when planning for a mortgage. How Much Can a Car Payment Cost You? Maybe Over $100,000. Defining exactly how much a car payment will impact a buyer’s home affordability isn’t something you can do in a vacuum. It depends on income, other debts, interest rates, and a host of personal financial factors. That said, looking at a few different analyses can give a clear sense of just how significant even a moderate auto loan can be. According to Mortgage Research Network , each additional $100 in monthly car payment can reduce a buyer’s home-buying power by roughly $14,000. For example, a $600 car payment could potentially lower the maximum home price by more than $80,000. A similar analysis from Refi.com finds that every $100 in car payment reduces mortgage-qualifying potential by about $15,400. At that rate, a $600 monthly payment could shrink a buyer’s mortgage-eligible price by nearly $90,000, depending on other debts and financial circumstances. And last, but certainly not least… Realtor.com suggested that a $430 car payment could reduce a borrower’s mortgage borrowing power by as much as $100,000 in certain situations. To put this in context, the average monthly car payment in the U.S. for a new vehicle is around $700, while the average for a used car sits closer to $500. And that’s just one vehicle—many households carry payments on multiple cars. When you start stacking those payments, it quickly becomes clear that the vehicles in your driveway can have a surprisingly large impact on the home that driveway leads to. Buy the Car You Need—but Know the Home It Costs You Seeing how much even a single car payment can reduce homebuying power makes it all the more obvious how critical it is to think carefully about buying a car not only during the home buying process, but also before you even start house hunting. For most buyers, it’s not about forgoing a necessary vehicle, but about making choices that preserve as much buying power as possible. That could mean opting for a used car purchased with cash, choosing a lower-cost vehicle, or delaying a second car until after closing. For others, living in a walkable neighborhood or one with good public transit can reduce the need for multiple vehicles altogether. Even small adjustments—like refinancing an existing auto loan or paying down debt before applying for a mortgage—can add tens of thousands of dollars to what a buyer could afford. Every decision around transportation affects the home you can realistically buy. With that perspective, you can make informed choices that balance your daily needs with long-term goals, helping ensure that your car payments don’t shrink your home-buying budget any more than necessary. It can also be helpful to connect with a local real estate agent and a mortgage professional early on—even if you’re not quite ready to buy. They can provide guidance specific to your situation, run the numbers for your income, debts, and potential car payments, and help you make informed decisions before taking on any new financial obligations. The Takeaway: Car payments can significantly reduce how much home a buyer can afford. Even a modest auto loan can translate into tens of thousands of dollars in lost purchasing power—and households with two or more car payments feel that impact even more. The more you understand how these costs interact with mortgage approval, the more control you have over your homebuying options. Whether that means choosing a lower-cost vehicle, waiting on a purchase, refinancing an existing loan, or exploring walkable, transit-friendly neighborhoods, small decisions can have big ripple effects. If you’re thinking about buying a home in the near future, looping in a local agent and a mortgage pro early can help you map out the smartest path forward.